In 2019, the European Central Bank (ECB) conducted a study on the payment attitudes of consumers in the euro area. The study called SPACE assesses consumers’ use of cash and non-cash payment instruments at the level of each participating euro area country and for the euro area as a whole.

As SPACE was conducted in between mid-March 2019 and mid-December 2019, 41,155 respondents in 17 euro area countries reported their transactions in one-day payment diaries. The scope of SPACE includes purchases at the physical point of sale (POS) and person-to-person (P2P) payments, as well as payments made remotely (i.e. for online shopping, telephone orders and mail orders, bill payments and recurring payments).

SPACE also explores the factors influencing individuals’ payment attitudes and behavior. Such factors are consumers’ self-reported payment preferences, as well as consumers’ access to and merchants’ acceptance of payment instruments.

Increase in the preference of cashless means of payment

When asked which means of payment they would prefer to use in a shop if they could choose, nearly half (49%) of the respondents answered that they would prefer cashless payment options, such as cards, whereas only 27% of them prefer cash. About one fourth (24%) said they were indifferent as regards the preferred payment instrument.

Regarding former studies conducted in 2016, the self-reported preference for cash in the euro area has dropped from an average of 32% in 2016 to 27% in 2019. This coincides with an increase in the stated preference for cards and other cashless payment instruments (from 43% to 49%) and a slight decrease in indifference (from 25% to 24%).

Results of an ad hoc survey from 2020 (IMPACT) show, that the greater preference for cashless means of payment seems to have continued during the pandemic in 2020. Owing to methodological differences, the results of IMPACT and SPACE are not entirely comparable. Still, the results give a rough overview, that the stated preference for cashless means of payment has increased to 54%, whereas the stated preferences for cash has decreased to 25%.

The share of respondents who expressed a preference for cash exceeded the share who preferred cards or other cashless means of payment in only four countries – Cyprus, Germany, Austria and Malta. At the other end of the spectrum, in Finland, Belgium, the Netherlands, Estonia, France and Luxembourg, well over two-thirds of respondents said they preferred cards or another cashless means of payment, with only a relatively small share expressing a preference for cash as a means of payment.

Huge increase in the access to contactless payment methods

Consumers are also increasingly gaining access to other payment methods than cash. In 2019, 58% of respondents reported having access to e-payment solutions, such as PayPal. 28% of respondents also reported having one or more mobile payment apps (e.g. Apple Pay) installed on their phones. Only 3.6% of respondents reported having access to crypto assets, such as Bitcoin or Ethereum. The share is highest in Germany (7%) and Cyprus (7%).

The impact of consumer age and education

Age plays a role not only in actual behavior, but also in stated preferences. The age groups 18-24 years (28%), 55-64 years (29%) and 65+ years (33%) have a greater preference for cash than those aged 25-54 (22-23%). The opposite can be seen for card preference.

Also, younger respondents were much more likely to have access to both internet payment methods (66% of respondents in the 18-24 age group) and mobile payments (43% of respondents in the 18-24 age group).

On average, rural respondents (29%) and those with a lower level of education (36%) reported a stronger preference for using cash than respondents living in urban areas (24%) and those with a higher level of education (19%).

Respondents with only primary education had much less access (18% for e-payment solutions and 8% for mobile payments) than those with a higher level of education (above 60% for e-payment solutions and 25% for mobile payments).

Cash as payment option by country and POS type

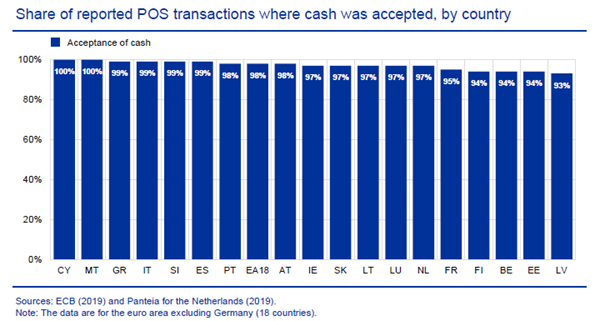

In the survey, respondents were asked to indicate for each payment whether any other payment option than the one they used would have been accepted. In general, it can be said that cash is still widely accepted in all countries, as shown in the chart below. Owing to a lack of data for Germany, conclusions can only be drawn for the other 18 euro area countries. On average, in these 18 countries, 98% of the reported transactions could have been made using cash, with the lowest share of cash acceptance in Latvia (93%), Estonia (94%), Belgium (94%), Finland (94%) and France (95%).

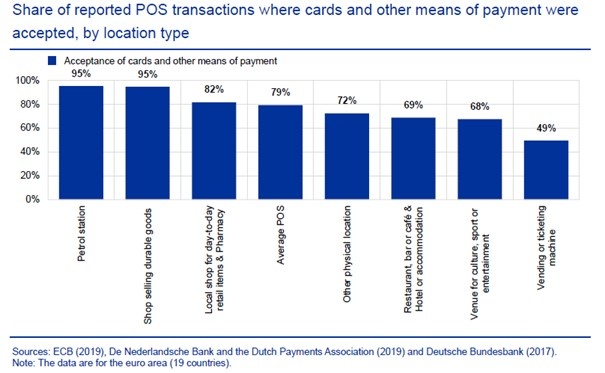

The locations where cash payments were most often not accepted in the euro area (excluding Germany) were petrol stations (9%) and culture, sports and entertainment venues (8%). This could be due to the fact that many petrol stations are unattended either 24 hours a day or at night and it is becoming more common for sports and entertainment venues to use reloadable cards or tokens which have to be bought in advance. The cash acceptance rate in other locations was reasonably high, as shown in the chart below.

Although only nearly a third of respondents declared that their most preferred payment instrument is cash, more than half of euro area citizens deemed it important (22%) or very important (32%) to have cash as a payment option, while one fifth of respondents considered cash neutral (21%) and the remainder considered cash not important (11%) or not important at all (13%). Still, more than half of euro area citizens consider cash important, even if they pay less with cash over time and generally have a preference for cashless means of payment.