A new International Data Corporation (IDC) study confirmed that cloud is the major disruption factor in the EMEA infrastructure hardware market, accounting for a growing portion of hardware spending and exerting influence on hardware architectures and vendors' strategies.

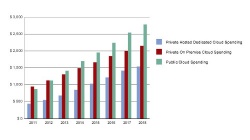

The overall investment in hardware for cloud environments in EMEA is expected to exceed $4 billion in terms of user value by the end of 2014, with a strong 19% YoY growth. 15% of the infrastructure spend in EMEA will be related to cloud environments in 2014, versus only 8% in 2011. This will grow to more than 22% by 2018.

The study, released in July 2014, presents the usage of infrastructure hardware elements in different types of cloud environments in EMEA: on-premises private clouds, hosted private clouds, and hosted public clouds. It includes historical data for cloud hardware spending in 2011–2013 and forecast data for 2014–2018. Hardware segments included are servers, external storage, datacenter networking gear, and security appliances. Server shipments and storage volumes estimates are also included.

"Along with Big Data, social, and mobility, cloud represents one of the four pillars of IDC's 3rd Platform vision — the new paradigm of IT usage that is revolutionizing the way technology is adopted in commercial and consumer environments," said Giorgio Nebuloni, research manager, IDC EMEA Enterprise Server Group. "The rise of cloud has triggered a revolution in the hardware market. While white-box and few large OEMs fight to absorb the surge in demand for public cloud, most incumbent hardware players invest heavily in offerings enabling on-premises and hosted private cloud environments, such as integrated systems, high-end networks, and high-performance storage."

"In the longer term, IDC expects greater adoption of hybrid cloud with benefits for both private and public consumption. Hybrid cloud allows customers to retain sensitive data behind a corporate firewall while still taking advantage of cloud-related lower costs," said Mohammed Hefny, senior research analyst, IDC EMEA systems.

Further Findings

- IDC estimates that $3.4 billion was spent on hardware going to cloud environments in EMEA in 2013, up 21% compared with 2012. This led to an increase in the penetration of the overall infrastructure hardware spending in dollar terms, which was flat at $26.3 billion in 2013 compared with 2012.

- The main business drivers prompting cloud adoption are closely related to its advantages in terms of easy scalability, agile mobile applications support, and lower total cost of ownership (TCO) — as well as regulatory compliance, backup, and archive — while Big Data analysis appears to contribute in minor, albeit rising, proportions.

- In 2013, 42% of cloud hardware spending was absorbed by public cloud environments, 38% by on-premises private clouds, and 20% by hosted dedicated private clouds. IDC forecasts that hosted private and public clouds will go fastest in the coming years.

- Penetration varies strongly by country, and it is more advanced in Western Europe than in emerging EMEA markets. In northern Europe, hosted private and public cloud deployments have been accelerated over the past two years, driven by large multinational providers especially in business to consumer environments.

Source: International Data Corporation (IDC)

{kind=link}